We could add $100,000 to millions of retirements. So why haven’t we?

The answer lies in outdated infrastructure in an industry slow to change, even when the upside is obvious.

Most people saving for retirement think about one number: The balance. Whether it went up or down, or roughly what trajectory it needs to follow before they stop working.

But what almost nobody thinks about is the infrastructure sitting between their savings and that number. The systems that calculate the value of their fund every day, process every transaction, reconcile every position, and produce the reporting that tells them how they’re doing.

That infrastructure is invisible by design. It is also, as I recently learned during an interview with FundGuard co-founder and CEO Lior Yogev, badly out of date.

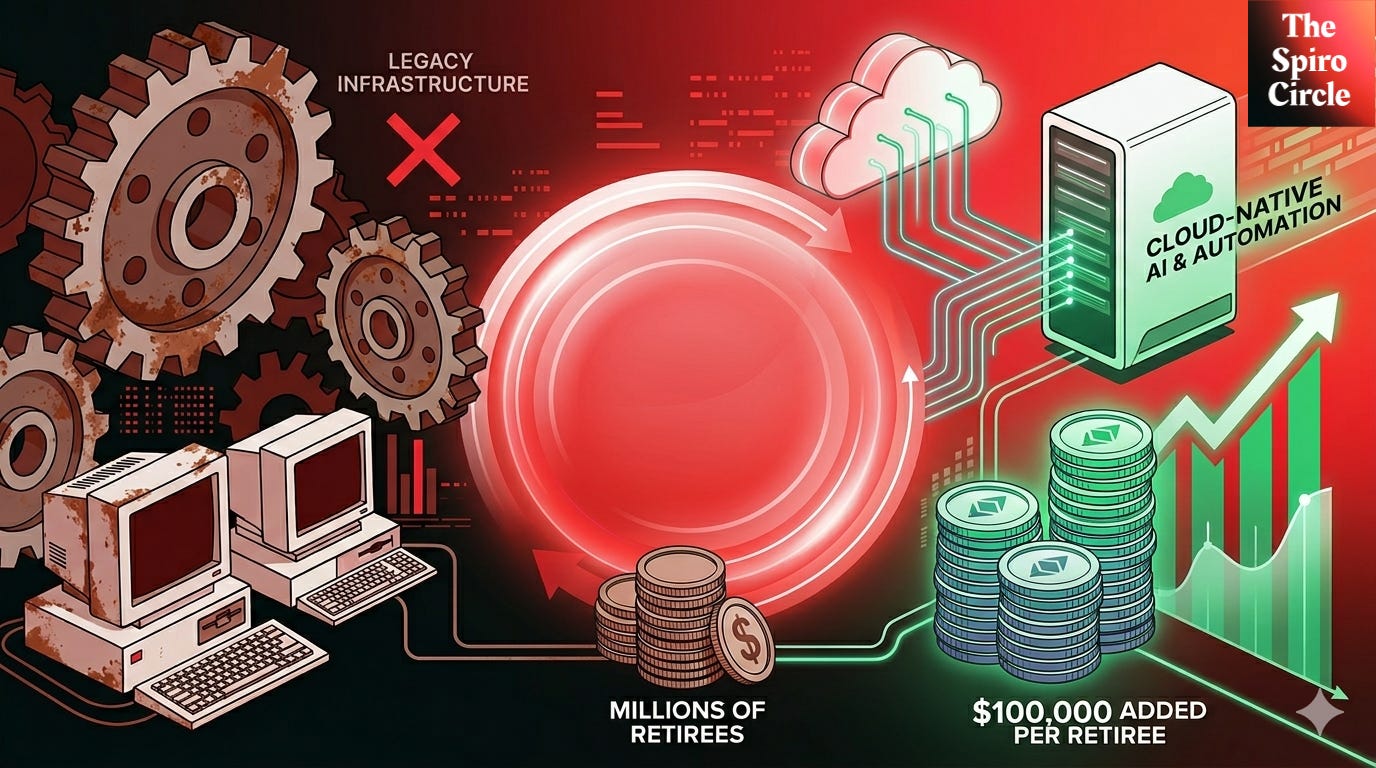

“More than 100 million people in the US alone save for retirement through mutual funds,” he told me during a recent episode of The Spiro Circle, in collaboration with Forbes Israel. The company builds core technology for the asset management industry and was selected for the Forbes Next Billion Dollar Startups list.

He is describing a 401(k).

There is a direct connection between back-office technology and retail investor outcomes, even if it’s never labeled as such. Running a mutual fund is not cheap. Analysts, offices, compliance teams, legal… the operational costs are substantial. Those costs are ultimately priced into the fees charged to investors, typically expressed as an expense ratio. The lower the cost of running the fund, the lower the fee can be, and the more of the return the investor keeps.

Legacy fund administration systems inflate those costs by design because they were built in an era when human processing was the only option for tasks that software should now handle automatically. And the software to do that exists.

If technology can shave even 0.1 or 0.2 percentage points from a fund’s operational costs by removing much of the human labor cost (the kind of reduction that automated infrastructure makes possible), it can translate, compounded over a working lifetime, to between $50,000 and $100,000 more per person in retirement. “While you’re not getting super rich by having another $100,000 in retirement, for most people, that is a huge, huge difference,” Yogev said.

The difference between retiring comfortably and retiring with constraint, for millions of people, is a technological one! And yet it has a known solution for a known obstacle: inertia.